National Australia Bank (NAB) demerged Clydesdale Group (CYB) in early 2016. Clydesdale has been a perennial thorn in the performance of the group. We do not have a position in NAB but are keenly watching ANZ. On a macro level we are more cautious on the financial institutions due to concentrated mortgage and housing market exposure.

The proposal give us a reason to take a closer look at NAB as well as CYB. After all CYB standalone is big enough to be included in the ASX 200 Indexes with initial indicative market capitalization of $4 billion.

The bank will also be included in the FTSE 250 during the June rebalancing period.

The goal of a demerger is to simply the businesses and create value through allowing the Australian business to focus on the Australian Banking sector. The UK management then can just focusing on managing the business directly instead of reporting to an Australian headquarter.

CYB can be attractive for those that want to UK financial exposure in the portfolio. It is will known the Australian banks are facing a number of issues that will provide headwind for future earnings. This included higher capital requirement, over exposure to real estate sector. House prices in Sydney and Melbourne can be considered stretched by any measure.

CYB LSE Listing

On a macro level, given where the Australian dollar is trading. CYB will be a pure play UK bank listed on the ASX. We question if owning CYBG listed on the Australian exchange is the best means to gain exposure to the bank.

In the event of stronger AUD, CYBG would under perform relative due to FX movements but irrespective to the performance of the underlying business.

For investors with a permanent allocation to UK market, owning the LSE stock is the way to go. This would largely eliminate the currency risk as long term FX exposure can be unwound at time of your choosing.

IPO Price

NAB has given initial indicative price for 25% of the offer than will be sold directly to the institutional investors. The remaining 75% outstanding shares will be distributed as in specie directly to current NAB shareholders.

CYBN Price Original Pricing Range: $3.50 to $4.70 AUD (175 pence to 235 pence). It settled at $4.00 per share.

The above indicative IPO range implies a significant discount to the tangible assets on the balance sheet from 0.56 to 0.76. This can provide an opportunity for investors with a value focus. This leads to the question of how confident with are with the book value.

Australian Banking Sector Performance

[visualizer id=”1580″]

Chart above shows the year to date share performance of CYB and big 4 Australian banks. CYB has out performed the big 4 banks so far.

Financial Overview

Banks are traditionally measured by price multiple of the book value of the tangible assets. Importantly because banks are leveraged businesses, shareholder equity on the balance sheet act as cushion for depositors is a critical measurement of bank capital adequacy.

As we saw during the financial crises, during periods of panic. High leveraged banks are the first to go out of business.

- Shareholder capital will make up 13.2% of Clydesdale capital (CET1 Ratio)

- NAB to maintain just sub 10% Basel III Common Equity Tier 1 Capital

- Currently there is a 2.1 billion pound coverage for legacy losses in which 1.15 billion has been indemnified by NAB (perpetually on specific legacy issues – PPI, IRHP and FRTBLs)

- Future losses will be shared between CYB and NAB based on a preset ratio of 90.3%/9.7%

The business is being spun off because the current NAB management have had enough of the continue under performance. Some common metrics highlight these issues:

- Net Interest Margin (NIM) which is the net margin between the amount it pays depositors and the interest it charges on the loans is steady at 2.2%

- Cost to income ratio is way too high at above 70%. This is in contrast to NAB it self which will have 41.9% from 50%.

- Impairment or bad debt charge as % of customer loans looks ok at 21bps

- ROE is terrible at 5.1% in 2015 down from 7.7% in 2014.

Given the low ROE, no wonder NAB is spinning off the company at a severe discount to Net Tangible Asset.

CYB Business Overview

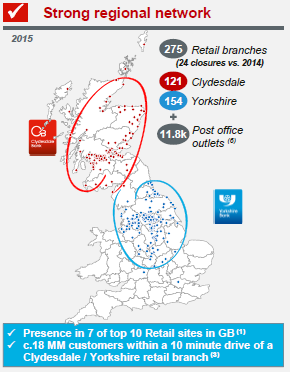

Regional Branch Network

CYB maintain a regional branch network is located in the Yorkshire, North East and North West of England.

Source: Company

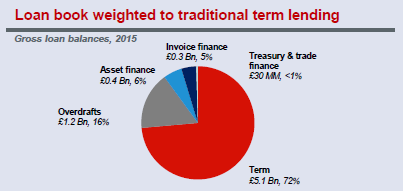

Loan Product

Target customer for the bank are retail and SME lending.

SME lending book segment shown below. Product segment shows more than 70% of the lending book are term loans followed by overdrafts then asset finance.

Source: Company

From fist look Clydesdale is a turnaround story. If management cut cost to income ratio then it could materially improve ROE without additional revenue growth. However given where we are today the high cost looks structural and will need time to cut.

Currently going through the docs and will update this post as we get a better picture of the proposal. Format will be done in similar vain to South 32 demerger and Atlassian IPO.