Our Sydney Property Forecast is cautious on further house price increases in the short and medium-term. Sydney is known for its beaches, food, and weather, with a quality of life on par with New York, London, Hong Kong, and parts of Canada and one of the most expensive residential real estate markets globally.

Sydney’s potential housing bubble was deflated between 2017 and 2019 when the banks pulled back financing during the onslaught of apartment supply from the last residential development cycle.

On the surface, the housing market was already on a backfoot just before the first wave of Covid-19.

The combination of strong underlying residential fundamentals and developer financing pullback will keep any fall in house and apartment prices in check.

We have gathered some interesting charts to highlight the key drivers of a negative to a stable outlook for the Sydney real estate market.

Our property market forecast for Sydney sees the market following a classic pattern from other house slowdowns worldwide. The run-up in prices leading into 2020/2021 will result in deflation after the boom. The real estate market will see a slow and steady decline rather than a sharp fall in real estate prices.

We are cautious in our property market forecast, and the slow down in Sydney house price growth will have broader implications across the NSW and Australian economy. The upside to our prediction is that even in a weak outcome, we still see the Sydney real estate market to perform better than other markets such as Melbourne and Brisbane property market.

Sydney House and Apartment Price Growth Recovering From pre-2020 Levels

The chart is courtesy of Knight Frank Research shows the performance of the Sydney residential property market over the last 3 years.

The Sydney house and apartment prices trend show that the property market peaked in early 2017 and saw an extensive period of weakness lasting over two years between 2017 and late 2019. During this time, the vacancy rise reflects the significant increase in apartments’ completion in the inner Sydney metropolitan region.

Notably, the price changes show that the market started to recover with price increases in the last quarter just before the onset of Covid-19.

During the mining boom, the strong Western Australian economy supported interstate migration inflows, which has reversed in the last two years. As people move back from WA, the pace of population growth pushed up demand for residential property.

Not coincidentally, the run-up in housing value in the last cycle happened after the previous mining boom collapse. The resulting interstate migration from the west coast to the east coast driven by jobs directly contributed to pushing up house values in the eastern capital cities.

The Reserve Bank of Australia also helped the boom when they reduced interest rates to a generational record low.

Bank lending will affect the Sydney property market in the future.

Real estate is a leveraged asset class. Either investing directly or indirectly in real estate through the Australian real estate investment trust. It is a primary driver of middle-class wealth not because real estate returns are better than equities or bonds but also the few only avenues where investors can purchase assets using enormous financial leverage every day.

For example, a typical Sydney House market median value of $1 million, if the investor borrows 90% of the funds with $900k mortgage. The $100k deposit or equity in the asset is leveraged 10:1 leverage.

If you use a “Conservative” deposit rate of 20%, this is still 5:1 leverage. You are buying an asset that is valued five times your equity contribution.Leverage can be used in equity investing with a margin loan, but it is uncommon to be above 50% or more than 2:1 leverage ratio.

The common wisdom is that the illiquid nature of the investment offset the higher leverage and work in investors favor as price falls are only realized when the asset is sold. However, his is only true for owner-occupiers.

If there is a significant fall in unit prices for investors, the bank may require additional equity if the loan is up for refinancing. If prices fall more than the equity and with no other capital injection, the banks will pull the plug.

Australian residential property has little or no securitization market since the GFC. The banks are in the driver’s seat in the market in lending funds for residential real estate. Australia Prudential Regulation Authority (APRA) has been proactive in limiting the banking sector’s animal spirits in funding for residential real estate, primarily through slowing the rate of residential investment loan origination by the major banks.

A critical driver of our property market forecast is conditional on the access to credit and, in particular, the bank lending standards at the time.

By this standard with strong anecdotal evidence of more stringent credit flows, absurd stories still exist for investors that hold multiple properties across the Sydney house market. However, they are the exception rather than the norm.

From now on, we anticipate a slower rate of credit growth will put a lid on further price appreciation.

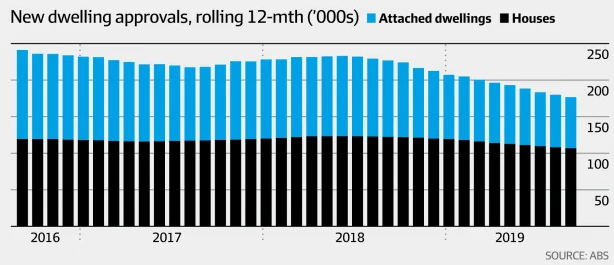

Sydney Property Prediction – Supply will fall off a cliff

Sydney’s historical residential property supply lagged demand. The limited supply was one of the main drivers of market price appreciation in the Sydney houses from 2013 to 2016. Over the last cycle, the shortfall was caught up by the rampant apartment unit supply concentrated in particular submarkets (Wentworth Point, Parramatta, South Sydney, to name a few). Shortages still exist in markets where supply is constrained, such as the northern beaches and areas where development approvals are always challenging to get through the council.

The apartment supply is coming off as we saw in 2018 and 2019. The uncertainties surrounding Covid-19 will hamper supply as developers will struggle to secure pre-sales and bank financing for the projects.

Our prediction is the Sydney apartment market will remain undersupplied for the foreseeable future as long as the economy is weak and unemployment is elevated. The limited supply will put a floor on further price falls soon.

There is an increase in residential supply from the shadow supply from the shift in AirBnB units to long term residential letting. While numbers are hard to come by, there are at least 130,000 AirBnB units designed for short-term accommodation and tourism, which is no longer required for 2020 and 2021. The transition of these units continues to depress the rental market.

We expect the Sydney auction clearance rate and volume to fall.

Foreign Capital Disappeared from Australian Property Market

Although history never repeats itself, it does rhyme. One drive of the market we are keeping an eye is the inflow of foreign capital into Australia.

Foreign money can create distortions due to regulatory constraints as foreign investors can only invest in the new housing stock. The resulting concentration of the purchases in new stock via pre-sales allowed developers to secure enough backing to satisfy banks’ funding requirements. In turn, they were one of the largest drivers of market supply in the last cycle and mostly concentrated in the gateway cities such as Sydney and Melbourne.

These are the additional factors that can affect the rate of capital flow.

- The NSW government increase in property stamp duty on foreign owners and higher land tax eroded the attractiveness of Australian real estate by foreign investors.

- The weak Aussie dollar limited the short term’s impact as the historically low exchange rate makes purchasing Australian properties cheaper from a foreign currency perspective. The benefit from the fall in the currency did not offset the near double rate of stamp duty on the purchase price.

The sum of the above means in the future, supply will be hampered as developers lost one of the easiest avenues of securing pre sales to start their projects, and while positive for long term prices, it is not ideal for future market supply.

Sydney House Price to Income Multiple

Like the price to earnings ratio used for stocks, real estate can be valued similarly to a multiple of either rental income or household income. The inverse of the multiple is called the cap rate. In this instance, the house value to median income is a measurement of housing affordability, while rental income is a measurement of value.

The Median House Price to income multiple for Sydney is on par with some of the world’s most expensive real estate markets.

How did the prices get to where it is today? The trend in house prices in multiple terms over the last 35 years shows that residential prices grew faster than income. The increase in Sydney housing prices was a story of multiple expansion, but multiple expansion is one-time occurrence and a finite driver of value. When multiple gets to a level where it can be no longer sustained, it will always revert to the mean. Interlinked to this is that the generational decline in the interest rates from the mid 1980’s means the long term mean have also gradually fallen.

Sydney real estate prices always contained a premium relative to the rest of Australia.

Downside risk to the Sydney property premium

If you take a typical residential property yield of 3% – 5%, then inverse, you can get a real picture of real estate valuation in Sydney. Under the scenario of 5% yield implies earning multiple of 20 times. Equivalently, for a stock to be priced at 20 times p/e ratio, there needs to be a great story to justify the future growth.

Record low-interest rates support the current high prices. The mistake is for investors to overpay, assuming the low rates are here to stay. If an asset is purchased at today’s level, the low-income yield is effectively locked in. An upward movement in rates would wipe out any cashflow growth unless rental income grows substantially from current levels.

Note it is difficult to lock in long term rates under standard mortgage products. Typical lock-in is five years at most, with 10-year money not very cost-effective.

Affordability indicator shows that the current market is stretched, and multiple expansion cannot go on forever. Asset owners are banking on income growth to justify the current high prices.

This is one of the most significant risks in our view to the real estate market in general, but as long as interest rates remain low and the economic shock of the Covid-19 is contained, then the multiple can stay high for the foreseeable future.

The risk in the future is that either household or the property rental income needs to catch up or price fall to compress the multiple, and in our view, price increases will be low in the future.

Sydney Rental Market and Vacancy Prediction

The only good news for a slow Sydney property market is for renters, which will be depressed for the foreseeable future.

SQM Research data shows that vacancy is already rising and will continue to risk as younger professionals move home due to Covid-19 and the increase in Airbnb supply.

The vacancy rate is expected to be the highest in the Sydney CBD where the market has the most significant reliance on the international student, hospitality employment and abundance of supply. We expect the Sydney CBD market weakness to be prolonged as long as the international travel ban persists and international students cannot enter Australia.

Interestingly Perth residential prices have been in a slump where natural demand has fallen away after the mining boom. Even as commodity prices have recovered, miners are still not investing in new mines. The rising vacancy rates have reduced apartment rents by almost 25%. The average price has fallen 10%, but this is the market average, and it would be worse it the fringe markets.

Impact of Rising Vacancy

Multiple expansions drove previous property price increases as a result of substantial investment flow into the real estate asset class. If the price to income multiple of property becomes too high, then the primary driver of value will be income growth.

The key question we ask is:

1) If income is not growing or even falls, would the underlying asset be worth the same? How much to an extent is future income growth priced into the price paid today.

2) What is the future price expectation if rental income (or return on asset) falls?

3) Given no growth in income, is the current yield on investment worth the risk?

Typical 3 – 5% gross yield on Sydney residential property does not look enticing with no rental income growth.

Sydney Property Market Forecast for 2021

Sydney property prices experienced strong growth compared to other major capital cities. Sydney has always had a premium to other capital cities, and recently the premium below out beyond the historical average from a relative price perspective.

Given the above factors, we consider the future of the Sydney residential market to be bleak. The prices are in the excess territory while supply is coming online to meet artificially low demand.

The slow down will be prolonged as it takes time for the market to absorb the supply and head towards more natural levels. The length of the slowdown means that future price growth will not be a repeat the past performance. A severe downturn in the residential market will affect the Australian economy with additional construction and services sectors.

Only because there is no hard landing scenario does not mean it will not be painful for real estate investors. As a result of covid, Australia had its first recession in 30 years. The leverage built into the system is larger than most expect, and any minor shakeout will have far and wide consequences across economic sectors outside the real estate industry.

The collapse of the Japanese and recent US real estate bubble showed consumer sentiment dropped significantly. We would expect any slow down to be the same in Sydney.

From the borrowing perspective, standard mortgage products are full recourse rather than limited recourse seen in the US residential lending market. People cannot just walk away from underwater mortgages. Interest payments, albeit lower in a downturn scenario, will still have to be paid.

Discretionary spending will be the first to be cut. The experience from the GFC was spending at the Pub and eating out collapsed overnight. Business spending takes time to be cut due to planning and contractual obligations. As Covid-19 saw, Consumer spending can be stopped overnight.

The silver lining is that Sydney is considered a core market. The best assets will still do better than secondary markets like Melbourne and Brisbane fringe markets.

Investment Implications From A Slow Sydney Real Estate Market

A weak housing market will have broader implications across the Australian economy and the equity markets.

Cyclical stocks for specialty retailers and even the extent to which the consumer shares will be hit due to an immediate decrease in revenue magnified by substantial operating leverage in the business models.

Financial institutions will not escape unscathed, as we saw in the fall in bank share prices. We feel the degree of severity will not be realized until bad debt charges upward spike from current levels.

We would be keeping an eye on the commercial real estate markets. Asset values have been supported by secondary stock leaving the market. A strong residential market means that the highest and best use of B grade office buildings is tearing them down and convert to residential apartments. This has support prices on otherwise terrible assets in already weak markets.

A slowdown in the Sydney property market means that office and industrial sites would be price naturally on a standalone value, resulting in a pullback in some listed property trusts.