South 32 (ASX S32) was demerged from the BHP Billiton intended to unlock hidden value in the assets the market overlooked as a combined entity. The result is South 32 which is no small picnic which by its size is automatically included in ASX 50, the 50 largest companies listed on the ASX and large component of the ASX mining index.

The common perception is that BHP retained the tier 1 mines while hived off the lessor quality assets to S32. However the performance of the mid tier miner since the demerger shows the management has played the cards it dealt with very well.

BHP on the other hand retained the petroleum, iron ore and potash assets while South 32 included the base metal assets such as lead, nickel and zinc.

Energy assets in coal (energy and Meallurgical coal) as well as alumina and precious commodity silver producing assets.

The energy assets were the primary drivers of one of the largest write offs in corporate Australia since shows that while the underlying business can do well, management can still destroy value via mis allocation of capital.

S32 Share Performance and Dividend Yield

S32 returns year to date is broadly in line with market with BHP and Rio Tinto Shares.

S32 Dividend History

S32 has been paying dividends since 2017 on an interim and annual basis. The pace of dividend increase and falls are inline with the commodity cycle where the company can be generous during the boom and protect the balance sheet during the cyclical lows.

It is important to note due to the global nature of S32’s business. As commodities are priced in US exchange rate, this means that fluctuations in the AUD to USD even EUR to AUD exchange rate can affect its Australian reported earnings.

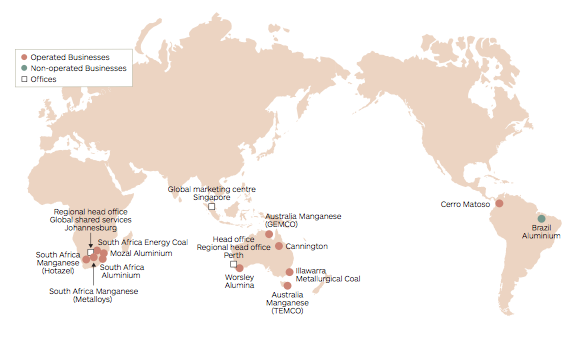

South 32 Global Presence

Map above shows the footprint of South32 globally and with most of its operations around the S32 parallel, naturally it called it self S32 when it seperated from BHP.

Highlight from the map above is the exposure to South Africa which does not have a great reputation for business and weak domestic outlook.

South 32 Commodity Exposure

S32 is primarily exposed to aluminum, thermal and metallurgical coal, nickel, lead, zinc and manganese.

South 32 Outlook

If the commodity down cycle bottom here then this is the best time to get in to S32 to gain exposure to these commodities. We are just unsure that we have seen all the weakness flushed out from the global economy and the covid recovery will be a slow slog in our view.

Solid balance sheet and management experience is a certain plus however a large portion of earnings will be cyclical and relient on the global commodity cycles.

Will keep an eye on this.