Dexus Dividend Dates 2017

Interim Ex-Dividend Date: 29/12/2016

Interim Record Date: 30/12/2016

Interim Dividend Payment Date: 28/2/2016

Final Ex-Dividend Date: 29/6/2017

Final Record Date: 30/6/2017

Final Dividend Payment Date: End of August

Dexus Dividend Dates 2018 (expected)

Interim Ex-Dividend Date: 28/12/2017

Interim Record Date: 29/12/2017

Interim Dividend Payment Date: 28/2/2018

Previous Note on Dexus and Investa Merger which was called off.

The sale of the Investa Platform is in the final stretch. Morgan Stanley has shopped the platform for over a year. CIC spent more than $2 billion for some of the best Core Office Real Estate in Australia and a platform for future growth. ICPF was sold and that leaves the listed Investa Office Fund last man standing.

Dexus is one of the largest Office REIT in Australia. Whilst there has been plenty of bidders only Dexus showed up to the party. It has a reputation for being acquisitive. Sectors like Office and Industrial is our preferred real estate asset class exposure verses residential and retail. If the merger is successful, it will the Australia’s largest commercial landlord and be the largest Office REIT in the ASX100.

Not only this has became one long sale process but with plenty of drama. The latest offer made by DXS was recommended by the independent board committee which was setup to evaluate the offers based on the best interest of the shareholders.

The management of IOF or portions of it has drafted a document that recommended current Investa Office Fund unit holders to vote no on the deal. Note this was not posted on the ASX but on Investa website.

Dexus offer for Investa

DXS offer is a combination of cash and script. Total value of the offer is dependent on the Dexus share price. The higher share price, the greater implied value for IOF shareholders.

- Standard Consideration: $0.8229 cash and 0.424 DEXUS securities per IOF Share. Shareholders have the option of choosing more cash or script with a scale back mechanism.

- Maximum Cash Payment of $4.1147 per IOF Unit (Total cash consideration capped at $505 million)

- Maximum Scrip Issued 0.53 DEXUS Securities (rounded to two decimal places) per IOF Unit (Total number of DEXUS Securities issued capped at 260.4 million)

Any shareholders that want 100% cash has the risk of scale back and issued Dexus Property Trust shares. For those that want complete cash certainty, investors can sell the securities on the ASX.

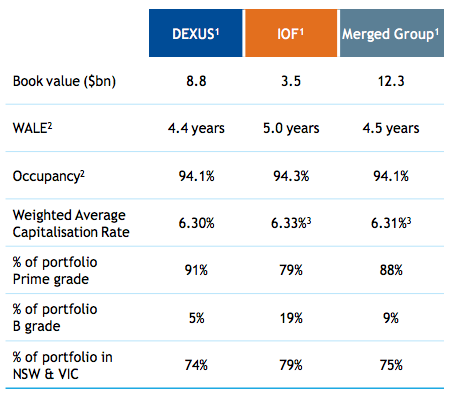

Dexus Portfolio

We took a snapshot from the presentation of what the merged portfolio would look like. DXS owns the premier Commercial Office portfolio in Australia. The assets cannot be replicated. Investa’s portfolio is almost at par with DXS.

IOF has a greater emphasis on Grade A and B rather than prime assets however given the tightly held nature of the asset class. Assets on this scale rarely change hands. It can be considered one of the most valuable portfolio of commercial office assets in Australia.

Whoever gains control of the portfolio would hold an enviable position to build on for the long haul. For those that missed out, even if you want exposure to the key Sydney and Melbourne markets, there will no alternatives.

Exhibit 1

The combined portfolio would be the largest single portfolio of premium and A grade office buildings in Australia. 75% of the portfolio would be in key markets of Sydney and Melbourne.

The downside of being so large is that it takes alot to move the needle. It is almost like Westfield where there needs to be multiple development projects to shift the dial in portfolio composition. Important to note development comes with a different risk profile to managing prime and grade A real estate.

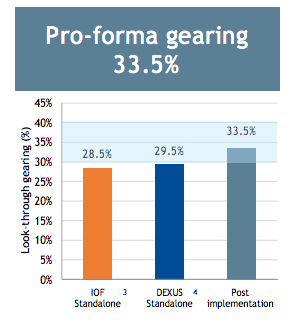

Dexus Balance Sheet

Based on where the office cap rates are trading we think we are closer to the current cycle peak.Current cap rate of 6.31% is pretty eye watering and cautious of funds that are leveraging up to buy assets in this environment even with record low interest rates and margin spread on debt.

Given there is a cash component as part of this transaction. The gearing level of the merged group is higher gearing relative to individual standalone REITs. Although the pro forma gearing is 33.5% is not eye watering, we would expect asset sales post transaction as management gets a better handle of the portfolio.

Post Transaction Playbook

The risk to the portfolio is not debt but asset values. Overall gearing can creep up either from greater amount of debt level as well as fall in asset values.

The issue is not quality of assets but the price. If the market stalls from here the downside risk of fall in asset value could put upward pressure on gearing. The risk could be offset by portfolio improvement through increase in occupancy. Each REIT has 5% vacancy but 5% vacancy on a $12 billion dollar portfolio is a very big number.

The playbook would be to value the portfolio post transaction and then be aggressive in filling those spaces. The value of a building is a function of future cashflows. While present DCF value would have an assumption on the current vacancy and expected rent. Given a REIT external valuation cycle could be 12 to 24 months.

Optimal approach is to confirm transaction valuation, be aggressive to get the vacancy filled even at discount to market rent. The goal is to get cash in the door and maintain earning momentum. The below market rent given could be washed out at next valuation period where market rate has improved better than expected or even improvement in future vacancy assumption.

We will also be keeping an eye on asset sales post settlement. A portfolio transaction means that there is also something in there that you wouldn’t have bought individually.

Investa Office Fund Alternative Offers

There are rumours that Mirvac could potentially take a tilt at IOF. Given MGR’s current management agreement with CIC, it has the relationship to work with CIC. MGR has a great prime and grade A office portfolio which shows it has the requisite skills to take on IOF.

If this scenario eventuate, we expect MGR to provide token equity as manager rather than wholesale cash and script offer. Although we have been wrong before (i.e Origin). However there is no offer on the table most likely because they are outgunned on price.

Cromwell IOF Stake

Cromwell Property Trust in a last minute play bought 9.83% stake in IOF. It is interesting how Dexus play this leading up to the vote on Friday 14th of April. Is there a deal to be made here where DXS convinces CMW to vote in favor of the merger in return for picks from the portfolio or is this a precursor for its own bid.

Outside chance is CMW ownership of Valad Europe gives it a unique angle in bringing a partner within its funds management business to take IOF private. Our view is that it is likely turn the heat of DXS to increase its own sweetener for IOF or do a deal post transaction.

CMW bought the stake at avg price of $4.24. Given where the IOF management has given FY17 guidance on earning, mid 21 cents and distribution yield sub 6%. The listed REITs are trading at frothy level. There is always a deal that calls the top of the cycle, is this it?