Australians have taken on record amount of debt to double down on housing in the current low interest rate environment. The million dollar question for Australian property investors this year is when will the interest rate rise? This is an important question as evidently the property market in the major cities has slowed materially and real estate being an leveraged investment means interest costs is usually the largest investment expense.

Melbourne and Sydney property markets are the most exposed to limits on foreign inbound travel as education is one of Australia’s largest export sectors. The pull back of tourism sector has really hurt the Brisbane apartments.

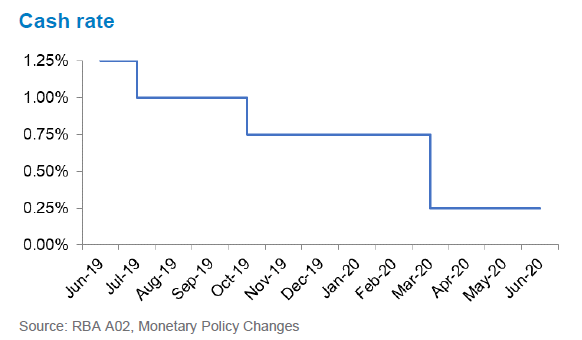

Reserve Bank of Australia Cash Rate

In the 12 month period leading up to Covid the economy was already slowing down and RBA reduced the cash rate twice in July and October 2019. In response to the anticipated economic slowdown as result of Covid the RBA further reduced the cash rate by 0.50% to historical low of 0.25%.

Based on current consumer and mortgage debt levels any rise in interest rates will put further pressure on retail sales and the economy with flow on implication to the stock market. We are watching several factors which will preempt any moves by the RBA to raise interest rates.

Australia Inflation Outlook is the critical factor

To understand when the interest rate will rise means we have to understand why the RBA change interest rates. It has a dual mandate of price stability and full employment but the market is always focused on the inflation mandate as it is a key driver of any increase in the cash rate.

Price stability mandate is not only in the context of current inflation but the future expectation or outlook.

The current Australian inflation rate has been trending below 2% which is below the RBA target band for awhile. What we need to have an lookout for is when the inflation expectation rises above 3%, then investors should worry about potential future rate rises as the Reserve Bank would be under pressure to carry out its mandate of price stability.

The current low inflation is a supportive of RBA not raising interest rates anytime soon.

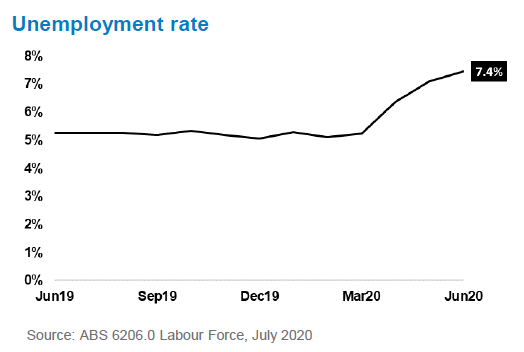

Continual Unemployment and Jobs Losses

Jobless rate is always on the mind of Australia’s central bank as it has a dual mandate of maintain low inflation and maximise employment rate.

In normal times this is paradoxical as employment growth is inflationary but in the current economic circumstances the increase in unemployment rate can be considered deflationary.

The deflation impact of the high unemployment again is another pressure valve offset on any pressure to raise interest rates.

We think even if the job market picks up in the short term it will not have any immediate pressure to act as the total quantum of the unemployment persons in Australia is just as important as the unemployment rate.

Australian Financial stability is the third pillar

In the pre recession period, the APRA cracked on mortgage lending by the banks as a safety value on the excess in the housing market. We think the forward outlook of Australian house prices plays an important role in RBA’s thinking but not in the way you would think.

Whilst a weak property price growth is preferred to a market going gangbusters. The health of the housing market is not as important is the secondary impact on the balance sheet of the Australian banks.

A severe recession would put pressure on the major Australian banks and flow on impact to access to credit by businesses. Ideally, the goldilocks outcome is a slow deflation of the house prices rather than a sharp fall so banks can adjust gradually by plugging any holes in their balance sheet by reducing their dividends.

What is happening to other economies?

Geographically Australia is an island (continent) but economically we are very much plugged into the global economy.

The performance of the economy is linked to other major economies for example 28% of Australia’s export is to China and the United State is still a very important trade partner. Therefore changes in offshore rates and subsequent impact on the Australian dollar will also play a part in the reserve banking decision process.

The rest of the world is experiencing record low interest rates as well with no visible path to get out of the deflation spiral. Japan has been in a zero interest environment for almost 2 decades and going forward it is looking like everyone is becoming Japanese from the monetary policy perspective rather than looking like Japan is the exception to the norm.

The Reserve Bank of Australia will make their decision on interest rates based on a combination of factors above. Change in interest rates will not be a mechanical decision but from qualitatively based on the economic context.