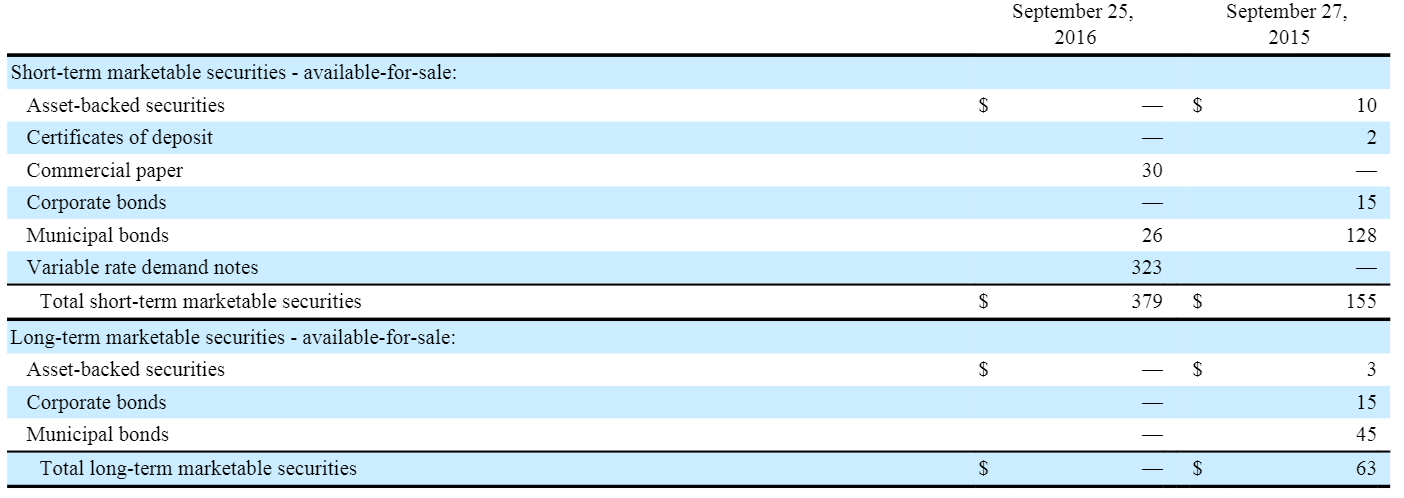

We don’t own that much retail in our portfolio with the exception of Woolworths. Wholefoods provides an interest angle to play the natural/organic food retail segment, and it looks especially attractive given the negative sentiment the market has on the stock. When we were looking at the most recent annual report, the table below shows that over the last 12 month it has shifted a large portion of its bond portfolio from vanilla municipal bonds to variable rate demand notes.

Given the size of the balance sheet and cash generation ability of the business it is not such a issue but interesting none the less.

Just as market goes in cycles so does products that investment banks create. We came across variable interest demand notes in our reading of the Wholefoods (WFM) 10K.

Basically, variable demand notes are short term floating rate municipal bonds. It has characteristics of both long term and short term bonds. While ostensibly it has a long maturity usually in the tune of 20 to 30 years, it also has a 1 to 7 day put option where the owner can put the bond back to the financial intermediary, usually an investment bank to be resold to others. The interest on these bonds are priced off the 7 day libor rate. The goal of designing a product like this is to create a sense of liquidity.

For those that have not been in the market during the financial crises, there were similar securities traded back then. It was called auction rate securities. However when the credit crises came about, the liquidity dried up for these products and the put option became useless. Years after the crises, there are still billions of these securities on issue.

Now at least the market has learned from the prior generation of these products by a credit enhancement tool in the form of a letter of credit which backed by another bank. If the financial intermediary cannot resell the bonds, then the line of credit provides support investor put the bonds to the LOC provider and investor could exit their position. The bonds becomes the LOC providers problem. At least this is an improvement upon auction rate securities where there were implied institutional support however when the market dried up, the implied support became worthless.