TPG Telecom is now undisputedly the top 3 telecom provider in Australia and it got to where it is today from implementing an acquisitive strategy. It bought iinet, the 2nd largest provider of DSL and National Broadband Network (NBN) internet service in Australia at the time and now following the merger with Vodafone it cement its position on the leaderboard.

Post the merger the combined entity remains in the S&P/ASX 300.

We do not own TPM at this stage however given the new scale and reach post Vodafone transaction, it has shown up on our radar. It is just the start of the research process and on our watchlist.

TPG FTTB Network

Ostensibly TPG looks like a mini Telstra but given the scale, more nimble in grabbing market share and product development. It has built on the base following the acquisition of iiNet and it was a key in reaching the scale it has today. Additionally, TPG continues to build its own fibre network in competition with NBN.

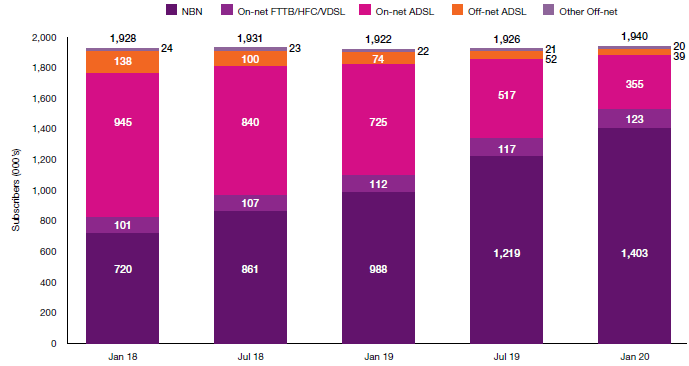

As NBN construction is near completion more of its customer base is expected to migrate to either TPG’s own fiber network or NBN and the drag from the migration would lessen the group’s margin. This is because overall NBN customers are less profitable than ADSL or customers using its own network.

Background for NBN: It is a national fibre network created by the government to ensure broadband infrastructure is available for all Australians. Fiber aim to cover 93% of population with rest serviced by satellite and wireless.

TPG through subsidiary Wondercom is building a competing fiber network. Instead of fiber to each premises, FTTB is Fiber to basement. This means that TPG is building a fiber network with a focus on high density areas in contrast to the NBN which by mandate has to cover everyone.

Building list of FTTB service shows the initial rollout is across east coast CBD locations. TPG FTTB network is required to provide wholesale service for other ISP retailers.

The ambition means that cash flow will be used to fund the rollout process or debt services charges.

The value is a competing network where high value customers is captured and ability to offer cheaper products verses NBN retailers. Once this gets scale, we feel it will propel TPG to a series contender for number 2 position in the telecom industry. This is our primary thesis for TPG. iinet acquisition is complement the wholesale service by allowing TPG to reach total customer scale but with a key eye on NBN retail.

Vodafone Australia Acquisition

It is no secret that TPG wanted to expand its offering by moving in the mobile segment to complement its existing broadband offering. At first it tried to build its own network unsuccessfully and instead went to the drawing board of acquiring the Vodafone network in Australia which is the 3 largest mobile operator after Telstra and Optus.

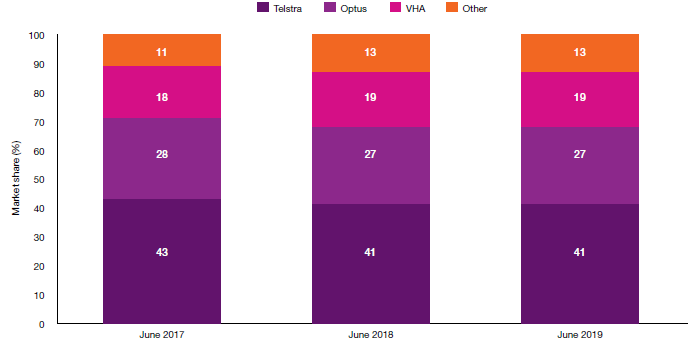

As direct consequence of the merger the combined group will have 17% of the mobile market share, 5.8 million mobile customers and have 25% of the fixed line broadband market and 2.1 million mobile customers.

The one thing we like the most about the business is that it will own a network that will be difficult to be replicated in Australia. It will have the second largest fixed voice and data network over 27,000km, an Australia wide mobile network with 5,613 sites on 4G and thousands of on-net fibre buildings. It owns the 7,000km submarine cable connecting Sydney to Guam.

Internet Service Providers (ISP) is a mature industry with entrenched telecommunications leader Telstra. Industry growth is single digit at best with smaller competitors focusing on taking market share from each other or from acquisitions.

At number 3 position across its main business line we think the business will grow above trend by taking business away from Telstra and Optus. However the immediate risk is to manage the expected customer churn which always happen after merger even though the business will retain both TPG and Vodafone brands. We suspect there will be 12 to 18 months of instability before the growth trend resume.

We will keep this on our list of shares to watch.

TPG Dividend Yield

Dividend based on the last 12 month of dividend over the current TPG share price.

TPG Dividend History

TPG dividends were below its peers even though it had a relatively stable business. A portion of its business were always in mids of transforming following acquisition and earning generated were kept by the company to fuel its growth.

We don’t expect this to change in the short term as we wouldn’t be buying the share for the dividends. Rather this will be a capital appreciation play as it captures more market share and increase its earnings.

TPG dividend dates are in May and November