Major economy interest rates across the globe peaked in the 1980s. As global economies become more intertwined with inflation ever declining as result of companies outsourcing manufacture jobs overseas. Interest rate has also fell in lock step.

We are still seeing the lasting impact from the financial crises which was primarily driven by leverage and the belief that house prices always go up.

After the financial and economic crises of 2007/8 which posed existential risk to the financial system. In the absence of fiscal policy, central banks have been the primary driver in keeping the economy afloat with their primary monetary policy tool being cutting interest rates.

As interest rates are at zero bound and cannot be reduced further. Policy innovation led by the United State Federal Reserve result in a shift to unconventional monetary policy, quantitative easing (QE). QE involve the central bank purchasing government bonds. Bank of Japan and European Central Bank with their own interest rates at zero bound have have also followed the footsteps of the Fed in implementing their own QE programs.

Negative yielding bonds definition

Government debt are issued at a fixed rate coupon. This means that bonds can trade at a premium to par or the principal value. When government bonds are traded, investors or traders bid up the price of the bond so much that the yield to maturity is negative. This means that at current prices the interest return from holding the bond is higher than the capital losses.

Total negative bonds outstanding – the greatest bubble of them all

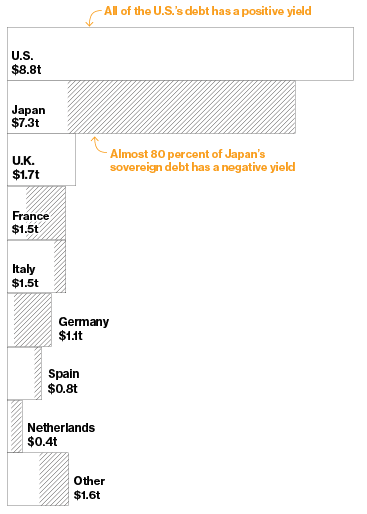

The chart below from Bloomberg breaks down the total debt outstanding and portion of that debt that is yielding negatively.

What is undeniable is that the US treasuries is the only major game in town. Japan is in its advanced stage of QE and was the first economy last majority of its bonds yielding negatively.

What is undeniable is that the US treasuries is the only major game in town. Japan is in its advanced stage of QE and was the first economy last majority of its bonds yielding negatively.

The same applies to German and Swiss bonds. The search for yield and safe haven means that the only remaining major European economies with positive yield are UK, France and Italy.

The bonds of these countries are not as attractive as Germany for a reason. Each country has a key factor holding investors back from Britain facing medium term economic uncertainty of Brexit, France with long history of sclerotic growth and Italy facing a potential banking crises.

Cause of negative interest rates and negative bond yields

We see the central bank buying government bonds as the primary driver of the negative interest rate. In the simplest sense, the original theory is that if the central bank buys the bonds, the sellers would then either invest in other asset classes or actually spend the proceeds on goods and services.

The issue here is the failure in the transmission mechanism where the sellers of bonds reinvested the proceeds back into other bonds either knowing that there is a massive uneconomical buyer which has to buy them at any price (central banks) or have a mandate to invest in bonds and like any good asset manager will not return capital willingly to its investors and forego the fee income.

These and other factors resulted in bonds in the last years beating equity performance at lower volatility. Paradoxically bond owners see past performance as indication of future performance.

The return of current bond holders are driven by capital gains. This has a tinge of a greater fool theory where assets are not priced by its fundamentals but the ability to sell at even higher price to someone else.

We consider the current period to be the generational high in fixed income assets. With a large portion of the market yielding close to zero, bond prices has a long way to fall at even a hint of inflation or change in interest rate expectations.

Fiscal policy is the solution to get out of negative interest rates

The start of QE by the US fed led to a record rally in commodities like gold, silver and copper as well as the fall in US dollar. With this completed, we predict that the US currency will outperform across major pairs and is in a multi year bull market.

The initial view is that QE will lead to inflation did not materialize. Inflation did not materialize because those could have spent the money have spent it and now have debt on house hold balance sheet. On other hand, QE did not have an impact on individual income which is the primary drag of the current malaise.

We agree with the argument that the weak economic recovery post the crises is driven by balance sheet recession. High households leverage coupled with limited income growth means that there is little appetite or room in increasing spending. The low interest rate helps but not enough across the economy to have a meaningful impact. This is the perfect instance of using fiscal policy to create demand and make up the private sector shortfall.

Government policy makers instead has focused on austerity which is the definition of insanity in a low growth world. Cut back of government spending resulted in fiscal cliff where the private sector in anticipation of government cut backs also reduced their own spending. The result is a lower and longer slump in growth.

Current implementation of quantitative easing programs by BOJ and ECB shows the limits of monetary policy. With limited interest rate differential between major economies, exchange rates like the JPY rally and fall against other currencies based on anticipation of changes to QE programs and risk appetite rather than core economic fundamentals.

The ECB and by implication the Euro is seeing similar results from QE. Our Euro forecast is that it will continue to be weak as result of continuing QE, political crises at its door step: Turkey and no green shoots in economic growth.