MG Unit Trust (MGC ASX) delivered an earning downgrade on April 27th. The first downgrade barely 12 months after listing on the ASX. It was one of the hottest IPO in 2015 when it debuted on the ASX at $2.24.

It is never a good sign that a company is going into trading halt as result of reviewing its full year earnings. Just ask ASX MEA.

- It announced a 30%+ earning downgrade from the original forecast included in the IPO PDS.

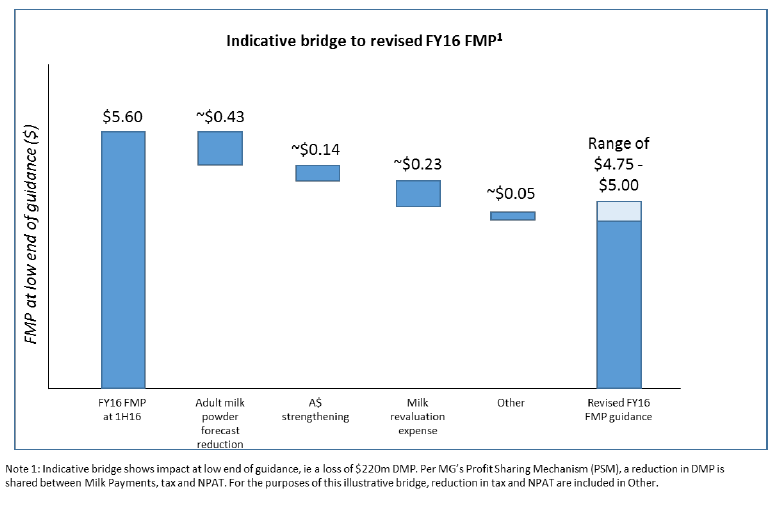

- Reduced earnings is a result of mix of lower farmgate milk solid price from $5.60 just made in February to between $4.75 to $5.00 and stronger Australian dollar.

- As a result, the distribution or dividend forecast which is linked to the Farmgate milk price is also cut to a range between 7.1 to 7.8 cents.

The earnings and dividends of Murray Goulburn are directly linked to the milk powder price. Therefore any downgrade in the commodity price would affect negatively the owners of the MGC shares. The company provided a breakdown for the cause of the lower Milk Price.

ASX MGC Share Price Performance Since IPO

The market reacted negatively where it took the Murray Goulburn share price fell 40% in one day. To rub salt into the wound, the company is facing a class action lawsuit which all shareholders whom owned the MGC trust up to the day prior to the downgrade will be eligible. It is getting messy here.

MGC share price made a nice recovery after the first earning downgrade however the announcement on 29th of July of losing the private label contract with Woolworths was another shock.

The contract covers milk, cheese, milk powder and cream and was worth $108 million a year. While it will not be material for the current year earnings, it will affect future earnings. This is offset this by a 5 year contract to Coles starting in February 2016 covering similar product breadth.

It was questionable that MGC was expected to keep Woolworths after signing the contract with Coles.

Intersting: see our 5 smart passive income ideas

Global Diary Industry

The global diary price has been under pressure in the last 12 month as result of Russian banning EU diary imports are retaliation of EU trade sanctions against Russia. This means that European diary productions need to go else where. Those new export markets are in direct competition with key Australia and New Zealand diary export markets.

The fall in New Zealand dollar reflect the global reset in diary price in the last 18 months.

The risk for ASX MGC is that the income on Murray Goulburn share price is directly linked to the domestic farmgate milk price.

The Australian price has held up relatively well compared to market rates across the globe. However a realignment of Australian price with global diary market poses a direct risk for MGC Unit Trust income. A decline in the farmgate milk price paid by Murray Goulburn will reduce the MG Unit Trust earnings and distributions.

There are moves by some parts of the industry in calling for a subsidy for farmers and additional tax of consumers so the producers can get through this difficult period. However we question the effectiveness of any subsidy for diary producers given the weak global diary price backdrop.

The trust has emphasized the shift to value added goods like Milk powder, UHT products and cheese. As well as focusing on key export market, China. The recent regulatory changes in China is not helping the change in emphasis for the group.

While there is no doubt that regulatory issues can be overcome by MGC. The regulation of milk imports into China is becoming more uncertain and under increasing regulatory scrutiny. Whilst increasing regulation can be addressed, it is the uncertain nature and unpredictability of future rules that is a risk for the suppler of importers.

Murray Goulburn share price did not fall as much as the pure export plays like Bellamy’s and Blackmore initially but the market will consider future earnings from this segment to be more riskier than before.