What is Lender Mortgage Insurance?

GMA is a single line insurance company offering lender mortgage insurance through the major Australian banks. It provides a direct exposure to the LMI segment of the insurance market with the other competitor being QBE which is operated as a diversified insurer.

Even as LMI is purchased by mortgage customers, the insurance contract protects the lenders from their default rather than for the borrower’s benefit. In the simplest sense the lender mortgage insurance policy payoff the difference between the realized value of the property after a mortgagee in possession sale and the remaining loan balance held by the lender. Borrower sign up for the lender mortgage insurance policy as it a condition of the loan approval for high loan to value loans.

GMA Shares

Genworth Mortgage Insurance is an interesting cigar butt idea where the GMA share price has been trading below book value. The company has been consistently returning capital either through fully franked dividends or share buyback over the last few years which showed an inflated dividend yield.

We looked at this awhile back and the company was in our view going through a self liquidation as the volume of new policy written was slowly declining vs the run off volume of its existing policies. And the Australian property market was undergoing a minor correction follow APRA’s crackdown on bank lending.

This is very different to the current environment in which GMA is operating in. There are signs that the company has found a footing in growing volumes again as the residential market has been performing well given the covid environment.

Key Risks Going Forward

The primary business of GMA is writing insurance contract or put options on Australian house and apartment prices. This means that ultimately the long term performance of the business is closely linked to the Sydney, Melbourne and Brisbane property markets.

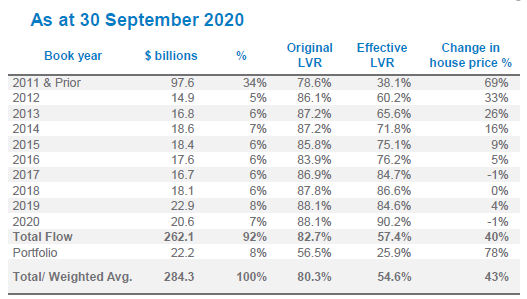

Insurance Policy Vintages

The table shows the breakdown of the insurance book by vintage and whilst the outstanding policies are broadly even over the last 10 years. The last column shows that house prices have been largely flat since late 2015 and 2016.

This means that the sum of all of the exposure from 2015/2016 to 2020 make up almost 40% of the policy vintage where there has been minimal increase in property prices or the buffer for its underwritten policies.

If there is a leg lower in the property market from today, there is limited additional cushion in the policy insurance book that you would have other wise from any value appreciation between the time the policy was written.

In our view the company is a leveraged play on the residential market where it will do well in cyclical up turns and magnitude worse in downturns.

GMA Dividend History

GMA final dividends are paid in August and interim dividends paid in March.